Oops! Something went wrong while submitting the form.

|

Research and development (R&D) tax credit calculation requirements and R&D credit percentages are unique from state to state. Most of our clients with operations in multiple states find it difficult to calculate R&D credits when operations span two or more states. Strike Tax Advisory experts will highlight how we can help you claim tax credits from federal and multiple state governments.

One thing that can help you understand the different state R&D tax structures is that there is commonality between the different states when it comes to tax credits. This occurs naturally since these are all derived from the federal tax credit structure.

Normally, the qualified research expenses (QREs) that a company incurs within the borders of a specific state are eligible only toward that state’s R&D credit. This includes payroll, products and contractors for the qualified research expense.

Let’s take the example of a company that has two facilities, one in Wisconsin and one in Illinois. Employees at both facilities are engaged in qualified research activities eligible for tax credits from federal and state governments.

The company calculates the QREs at the Wisconsin facility to be $300K, and the QREs at the Illinois facility to be $100K. The $300K of QREs occurring in Wisconsin would be eligible for inclusion in both the federal and Wisconsin credit computations. The $100K of QREs occurring in Illinois would be included in both the federal and Illinois credit computations.

Some states like Kentucky and Alabama have no R&D tax credits, leaving only federal tax credits as the incentive for research. If a company operates in two states, but only one of them has a state R&D tax credit, they will be able to file in the eligible state for state credit. When it comes to their federal filing, the company can claim all of their qualifying expenses and activities from both states for one big federal return.

Now comes the tricky part. Similar to the different federal computation methods, there will be multiple ways to compute a specific state R&D credit with varying percentages allowed as tax credits.

Generally, states have calculated the R&D credit in one of two ways. Either it will look at the increase in research compared to a base amount, or it will measure the amount of QREs that are above the average of the last three tax years. These are respectively referred to as the Regular Research Credit method and the Alternative Simplified Credit method.

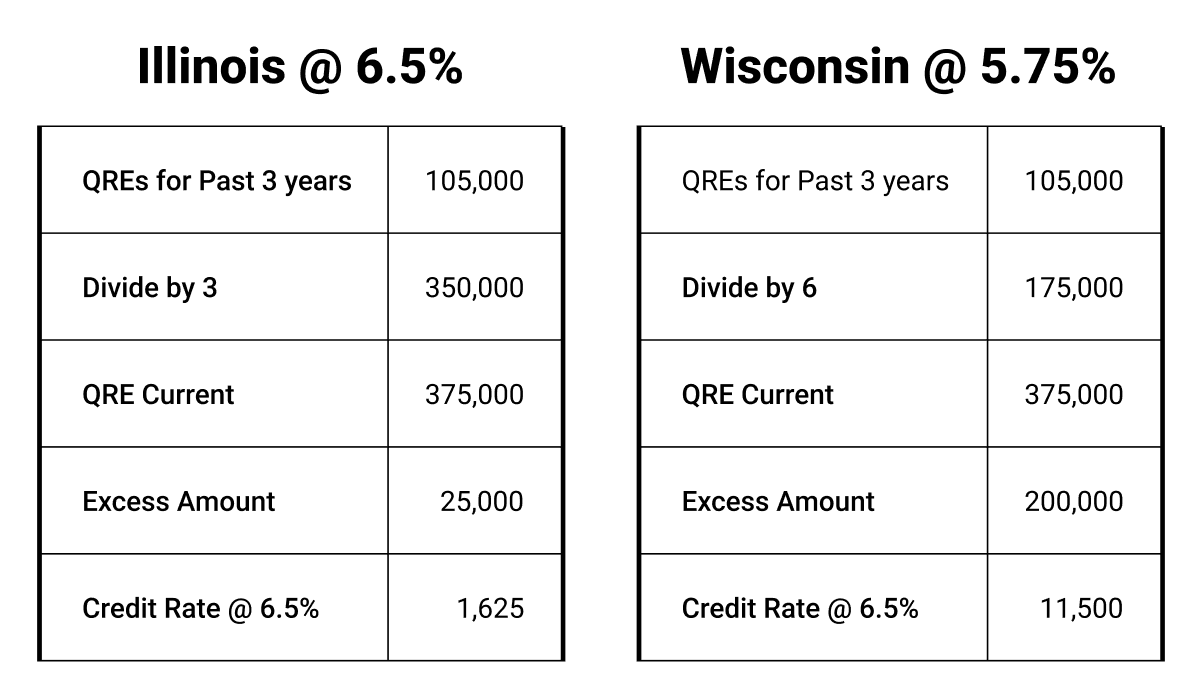

Here is a simplified side-by-side comparison of similar expenses computed using both the 2019 Wisconsin and Illinois computations, as an example.

Illinois has a higher credit percentage (6.5%) over the Wisconsin credit percentage (5.75%).

Wisconsin’s calculation compares the current-year eligible expenses to 50% of the prior three-year average. It’s easier to exceed than the Illinois computation that requires a company to exceed the average eligible expenses from the prior three years.

Some states only offer R&D credit to C-Corps, like Florida. Some states recognize carryforward credits, but other states, like Kansas, do not. Even though the state R&D tax credit is based on the federal tax credit, there’s still enough variety in state laws to keep tax credit calculations exciting.

California R&D calculations have a distinct difference from the federal tax credit. The federal government defines gross receipts as “total sales (net of returns and allowances) and all amounts received for services”.

California, on the other hand, defines gross receipts as the sale of “real, tangible, or intangible property held for sale to customers in the ordinary course of the taxpayer’s trade or business delivered or shipped to a purchaser within California”. Service-related receipts, rents, or interest are not included in this definition. The statute of limitations in California is also four years instead of three years, like it is in federal R&D filings.

In a few unusual cases, like Arizona, it’s not the percentages or calculations that make claiming the credit difficult. Arizona caps the amount of R&D funds it disburses. Companies that submit their claims first are more likely to receive the limited funds available. Timing, not calculations, matter more for a state like Arizona. Combined with additional state claims, this can make an R&D claim even more challenging.

If you’re a CPA, you can take a continuing education course to tackle a multi-state R&D tax claim, or you can reach out to a Strike tax specialist. We’ll make it easy for you to expand your services without increasing your workload.